Bitcoin Depot's 2025 Form 10-K hit EDGAR at 4:02 PM on March 18, 2026 — one day late, filed under the shadow of a two-sentence NT 10-K and a Connecticut emergency order that suspended the company's statewide operations nine days earlier. The 298-page filing is simultaneously the most complete disclosure Bitcoin Depot has ever made and, in the contrast it creates with everything that was not disclosed before, its most damning document yet.

Our original investigation raised questions about founder Brandon Mintz extracting $70 million while the company faced allegations of facilitating consumer fraud. The new filings don't just validate those questions. They provide the receipts. They reveal a company whose operating entity was failing state-mandated minimum net worth requirements while insiders negotiated bonus structures tied to extracting cash. They expose a litigation docket that exploded in size overnight — after years of near-silence in prior filings. And at the center of it all sits a single document, hidden for nearly three years, that functions as the Rosetta Stone of this investigation.

- $29 million in preferred dividends paid to BT Assets (Brandon Mintz's entity) — triggering $725,000 in bonuses for CEO Scott Buchanan under a secret compensation agreement

- Exhibit 10.32 — a July 2023 letter agreement tying Buchanan's pay to Mintz's distributions, hidden from two prior annual reports

- Connecticut DOB order confirming Bitcoin Depot Operating LLC failed minimum Tangible Net Worth in both 2022 and 2023

- $35.1 million raised from retail investors via at-the-market equity sales in 2025 while the balance sheet showed negative $16.5M equity

- 8 legal proceedings now disclosed — most absent or minimized in every prior filing

- 30–40% revenue decline projected for 2026, attributed to "compliance enhancements" — suggesting that a substantial portion of historical revenue relied on lax controls

Section 01The Rosetta Stone: Exhibit 10.32

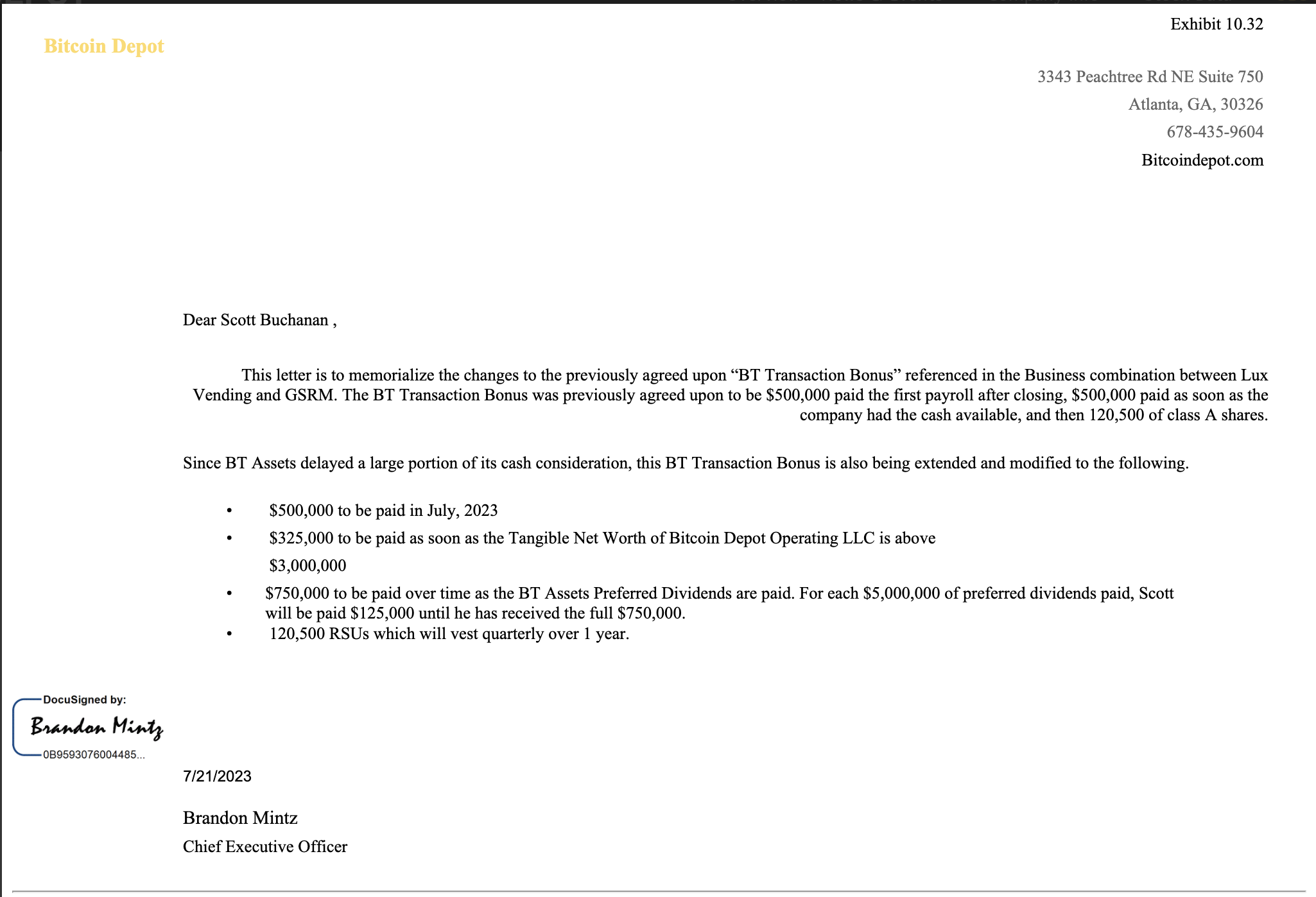

For the first time since going public in June 2023, Bitcoin Depot attached a letter agreement to its annual report that changes the math of this entire investigation. Exhibit 10.32 is a one-page document signed on July 21, 2023, by Brandon Mintz as CEO and addressed to Scott Buchanan, then COO. It restructures Buchanan's "BT Transaction Bonus" into three tranches, each of which encodes a separate financial incentive:

Plus 120,500 RSUs vesting quarterly over one year.

The third tranche is the smoking gun. Under its terms, every time Bitcoin Depot pays $5 million in preferred dividends to BT Assets — Brandon Mintz's controlling entity — Scott Buchanan personally receives $125,000. The 10-K's narrative compensation disclosure confirms: as of the filing date, $29 million in preferred dividends have been paid to BT Assets. Accordingly, Buchanan has earned $725,000 of his $750,000 maximum — paid for by the act of moving cash from the company to the founder.

The structural alignment is explicit. Buchanan's bonus was mechanically triggered by the same distributions that drained the company. He was not merely a bystander to Mintz's extraction — he was a contractual beneficiary of it. Mintz, as CEO and controlling shareholder, chaired the Compensation Committee that approved (or ratified) a bonus structure under which his deputy was paid for every dollar Mintz extracted from the company — a textbook related-party transaction executed under a governance framework the company itself acknowledges is exempt from standard independence requirements by virtue of Mintz's "controlled company" status.

The second tranche is equally revealing. The $325,000 payment is conditional on the Tangible Net Worth of Bitcoin Depot Operating LLC exceeding $3,000,000. When Mintz and Buchanan signed this agreement on July 21, 2023, the SPAC merger had closed just three weeks earlier. The going-public process would have involved full financial due diligence. The same 10-K that finally publishes this agreement also discloses that the Connecticut Department of Banking found Bitcoin Depot Operating LLC failed to maintain the legally required minimum TNW of $1,000,000 in both 2022 and 2023.

They set a $3 million TNW trigger precisely because they knew the company wasn't there. The question this document forces into the open: at the time this agreement was signed, did Mintz and Buchanan know that OpCo's TNW was below $3,000,000 — and if so, was the pending status of that $325,000 bonus payment deliberately structured to mask the company's license compliance status from investors?

Why was this document withheld for nearly three years? The July 2023 amendment was referenced in narrative compensation disclosure in the FY2024 10-K — the company disclosed enough in prose to show awareness of the agreement. But the underlying document itself was not filed as a required SEC exhibit until the 2025 10-K, filed March 18, 2026. Under Regulation S-K Item 601(b)(10), material compensatory arrangements with Named Executive Officers are required annual-report exhibits. The FY2023 10-K (filed March 2024) did not include it. Nor did the FY2024 10-K. This is actually a stronger claim than simple nondisclosure: the company disclosed enough in narrative form to show awareness, while simultaneously failing to provide the actual document as required under SEC rules.

Section 02The Insolvency Receipts: Tangible Net Worth and the Cash-Out Timeline

How bad was the balance sheet while these distributions were flowing? The publicly available SEC filings provide consolidated balance-sheet data quarter by quarter. The table below assembles the reported consolidated stockholders' equity and computes a tangible net worth proxy by subtracting goodwill and intangible assets.

| Period End | Source | Total Equity ($M) | Less: Intang. & GW ($M) | TNW Proxy ($M) | Regulatory / Documentary Markers |

|---|---|---|---|---|---|

| 12/31/2022 | FY2022 filings | $9.44 | $14.07 | −$4.63 | CT DOB: OpCo failed $1M minimum TNW |

| 06/30/2023 | Q2 2024 10-Q comparative | $2.97 | ~$13.32 | −$10.35 | SPAC merger closes June 30, 2023 |

| 07/21/2023 | Exhibit 10.32 | — not a reporting date — | Buchanan signs bonus agreement $325K trigger: OpCo TNW > $3M |

||

| 12/31/2023 | FY2023 10-K | $9.37 | ~$12.55 | −$3.18 | CT DOB: OpCo failed $1M minimum TNW |

| 06/30/2024 | Q2 2024 10-Q | $4.44 | ~$11.65 | −$7.21 | Equity sharply lower; cushion narrowing |

| 09/30/2024 | Q3 2024 10-Q | $1.25 | ~$11.34 | −$10.09 | Near-zero equity; severe balance-sheet stress |

| 12/31/2024 | FY2024 10-K | −$16.49 | $11.04 | −$27.53 | $29M preferred distribution to BT Assets $37.16M total distributions in 2024. Liabilities: $96.6M vs. Assets: $80.1M |

| 06/30/2025 | Q2 2025 10-Q | $4.70 | ~$10.30 | −$5.60 | Equity recovering from -$16.5M; still TNW-negative. ATM equity sales ongoing |

| 09/30/2025 | Q3 2025 10-Q | $21.00 | ~$9.90 | +$11.10 | First positive TNW after stock dilution proceeds. $35.1M equity raise absorbing losses |

| 12/31/2025 | FY2025 10-K | $11.83 | ~$9.52 | +$1.90 | $18.5M arbitration accrued pulls equity back down Buchanan earns $725K from dividend-linked bonus |

The trajectory is stark. At December 31, 2024, Bitcoin Depot's consolidated liabilities exceeded its consolidated assets by roughly $16.5 million. During that same year, $37.16 million in distributions flowed to BT HoldCo members — primarily BT Assets, Mintz's vehicle. The company was paying out tens of millions to its founder while, by its own reported numbers, it was balance-sheet insolvent at year-end 2024.

Under Section 18-607 of the Delaware LLC Act, a distribution is unlawful if, at the time it is made, the company's liabilities exceed the fair value of its assets. The 10-K's own balance sheet — liabilities of $96.6 million against assets of $80.1 million as of December 31, 2024 — raises the question of whether the distributions made throughout 2024 and 2025 complied with Delaware law. Whether the Up-C structure insulated any individual from personal liability is a material legal question this article flags but does not resolve.

A note on TNW as an investor risk: The loss of state money transmitter licenses can be catastrophic for the business — the company simply cannot operate in states where its license is suspended or revoked. Bitcoin Depot operates under 19 active state money transmitter licenses. Yet insufficient or negative TNW was never disclosed as a specific risk factor to investors in any prior filing. The Connecticut order demonstrates this risk is not hypothetical.

The $70 Million+ Extraction: Audited Breakdown

The headline "$70 million+" figure from our Part 1 investigation is referenced throughout but deserves an audited accounting in one place. Based on the 2025 10-K and prior SEC filings:

| Component | Amount | Period | Source |

|---|---|---|---|

| BT Assets distributions (2024) | $37.16M | FY 2024 | 2025 10-K (includes $29M preferred) |

| BT Assets distributions (2025) | $10.1M | FY 2025 | 2025 10-K (pre-restructuring) |

| TRA termination payment | $8.4M | May 2025 | 8-K (May 30, 2025) |

| Documented Form 4 stock sales | ~$16.4M+ | 2024–2025 | SEC Form 4 filings |

| Documented total | $72M+ | 2024–2025 | Excludes pre-2024 distributions |

Note: Pre-2024 distributions to BT Assets are not included. The total extraction since the June 2023 SPAC listing exceeds $70 million with room to spare.

Section 03The Insider Transaction Timeline

The Buchanan bonus agreement is the earliest documentary link between management's awareness of TNW as a metric and the insider-aligned cash extraction incentives. But the timeline extends through 2025 and into 2026, with insider trading plans adopted, terminated, and replaced during a period when the litigation and regulatory picture was deteriorating rapidly.

| Date | Insider | Event | Details | Significance |

|---|---|---|---|---|

| 07/21/2023 | Buchanan / Mintz | Compensation agreement | Exhibit 10.32: TNW + dividend triggers | Earliest documentary link between TNW awareness and insider payout incentives |

| 03/2025 | Brandon Mintz | 10b5-1 plan cancelled | Prior selling plan terminated | Unusual: plan cancellation followed by new plan two months later |

| 05/30/2025 | Brandon Mintz | TRA termination | $8.4M cash payment to Mintz | Press release framed as eliminating "$2.2M TRA liability" — the 8-K filed same day discloses the actual cash payment was $8.4M |

| 05/31/2025 | Brandon Mintz | 10b5-1 plan adopted | Covering 8,000,000 Class A shares | New formal insider-sale program, one day after $8.4M TRA payout |

| 09/05–22/2025 | Brandon Mintz | Form 4 sales (6 filings) | Sales under 10b5-1 plan; corrective filing 09/09 | Occurs during litigation buildup; BitAccess hearings ongoing |

| 10/07/2025 | Company | $15M offering priced | Registered direct offering | BitAccess arbitration hearings ran through October — undisclosed in offering docs |

| 11/24/2025 | Company | $18.5M award disclosed | BitAccess arbitration loss announced via 8-K | Disclosed after the $15M offering closed |

| 11/26/2025 | Brandon Mintz | Plan terminated + replaced | New 12M-share plan through Nov 2026 | Post-award, pre-Massachusetts AG filing |

| 11/26/2025 | Scott Buchanan | 10b5-1 plan adopted | 49,000 Class A shares | New CEO establishes his own sale plan on same day as Mintz |

| 12/19/2025 | Company | Credit amendment | Silverview: judgment default threshold raised $1M → $3.5M | Protects against BitAccess covenant breach; carves out "certain existing matters" |

| 01/01/2026 | Mintz / Buchanan | Role transition | Mintz → Executive Chairman; Buchanan → CEO | SOX Section 302 certification shifts to Buchanan |

| 03/09/2026 | CT Dept. of Banking | License suspension | Emergency C&D; TNW deficient 2022–2023 | Same day Bitcoin Depot files NT 10-K citing inability to file on time |

| 03/18/2026 | Company | 2025 10-K filed | 298 pages; Exhibit 10.32 first published | Material weaknesses disclosed; disclosure controls "not effective" |

Two dates demand particular attention. On November 26, 2025 — two days after the $18.5 million arbitration loss was announced — Mintz terminated his 8-million-share trading plan and adopted a new one covering 12 million shares, running through November 2026. Buchanan adopted his own 49,000-share plan the same day. Both insiders were establishing formal disposition programs at the precise moment the company's litigation exposure had become undeniable.

The December 19, 2025 Silverview credit amendment is equally telling. One month after the arbitration award and two months before the Massachusetts AG complaint, Bitcoin Depot raised its credit agreement's monetary judgment default threshold from $1.0 million to $3.5 million and carved out exceptions for "certain existing matters." The timing — six days before year-end, in the direct shadow of the $18.5 million liability — suggests management was actively managing the cascade of litigation disclosures to prevent a debt default event.

Section 04One Order, Two Hidden Liabilities: The Coin Cloud Connection

The 2025 10-K discloses for the first time a separate dispute with BitAccess minority shareholders, led by co-founder Moe Adham, seeking $0 to $10.4 million. This disclosure, when read alongside Adham's October 25, 2024 Ontario Statement of Claim and the already-disclosed $18.5 million Cash Cloud arbitration, reveals that what Bitcoin Depot had presented as separate litigation buckets trace back to a single alleged act.

In his claim, Adham alleges that on August 1, 2022, Bitcoin Depot directed BitAccess to terminate software services to Coin Cloud — BitAccess's largest customer, representing approximately 85% of its annual revenues — for anti-competitive reasons. When Adham refused to breach a court undertaking not to interfere with Coin Cloud's software access, Adham alleges that Bitcoin Depot unilaterally seized control of BitAccess's software and deactivated Coin Cloud's access over his objections. This, Adham alleges, necessitated an emergency hearing before Justice Hooper of the Ontario Superior Court, who granted an interim injunction restoring access temporarily.

In its public bankruptcy filings, Coin Cloud cited Bitcoin Depot's conduct as the cause of its insolvency before filing for Chapter 11 on February 7, 2023, with over $153.9 million in liabilities. (Coin Cloud's bankruptcy had other cited contributing factors, including a hack and alleged CMO fraud.)

Combined undisclosed exposure: ~$29 million. The Cash Cloud arbitration ($18.5M) and the Adham minority shareholder dispute ($0–$10.4M) both arise from the same alleged August 2022 cutoff directive. Neither was adequately disclosed in SEC filings until the 2025 10-K — over two years after the underlying events.

Adham further alleges that after ordering the Coin Cloud shutdown, Bitcoin Depot submitted financial data to valuation firm Alvarez & Marsal that excluded Coin Cloud's revenue — on the basis that Coin Cloud was "no longer a customer" — thereby depressing the fair market value of the minority shareholders' 20% interest from what Adham says should have been $8–10 million to approximately $4.4 million. The GSRM SPAC transaction agreement's Section 6.8 explicitly contemplated a post-closing BitAccess buyout, and GSRM's June 20, 2023 public disclosure stated the estimated value of the non-controlling interest at approximately $4.4 million. The obligation was acknowledged in the very documents used to take the company public; Bitcoin Depot now disputes whether the SPAC constituted a "Parent Liquidity Event" triggering the buyout.

Section 05The Disclosure Flood: What Changed and Why

The 2025 10-K contains a far longer and more detailed roster of legal proceedings than any prior filing. The contrast is not subtle. Earlier filings were thin to the point of omission; the 2025 10-K reads like a legal risk inventory that was opened all at once.

| Proceeding | Est. Exposure | When Filed / Initiated | When First Disclosed in SEC Filings |

|---|---|---|---|

| Canaccord Genuity (Canada) | $0–$23.0M | Jan 13, 2023 | Partially disclosed; OpCo added as defendant in 2024 |

| Byte Federal Trademark (FL) | Settled post-YE | Jan 20, 2023 | Not disclosed until 2025 10-K |

| BitAccess / Cash Cloud Arbitration | $18.5M | Commenced Aug 2022; hearings Dec 2024–Oct 2025 | Disclosed Nov 24, 2025 via 8-K (post-$15M offering) |

| Moe Adham / BitAccess Minority | $0–$10.4M | Active evidentiary phase | First disclosed in 2025 10-K |

| Iowa AG Consumer Fraud | Injunction + penalties | Filed March 2025 | Partially disclosed in 2025 quarterly filings |

| Massachusetts AG | Material; investor rescission sought | Filed Feb 3, 2026 | Disclosed as post-year-end event in 2025 10-K |

| Georgia Class Action (Data Breach) | TBD (26,732 customers) | Filed Aug 5, 2025 | Disclosed in 2025 10-K |

| Connecticut DOB License Suspension | Disgorgement + revocation | Order March 9, 2026 | Disclosed as subsequent event in 2025 10-K |

| Maine Settlement | $1.9M (paid) | Resolved Dec 2025 | Disclosed as resolved in 2025 10-K |

What Forced the Disclosure?

Three concurrent pressures converged to produce the most candid annual report Bitcoin Depot has ever filed:

Trigger 1: The CEO transition and SOX exposure. On January 1, 2026, Buchanan replaced Mintz as CEO. Under Sarbanes-Oxley Section 302, the certifying officer faces personal liability for material omissions. A new CEO inheriting a disclosure record riddled with buried lawsuits and hidden compensation agreements has a powerful incentive — legal and personal — to ensure the first 10-K filed under his signature is complete. Buchanan's new CFO, David Gray (appointed March 2025), would have shared that incentive.

Trigger 2: The BitAccess arbitration award. The $18.5 million ruling, announced November 24, 2025, was the first moment this liability became a determined, quantifiable loss. GAAP requires disclosure of probable losses once determinable. But the arbitration proceedings had been ongoing since August 2022 with hearings through October 2025 — hearings that occurred during a period when the company made no contingent liability disclosures in any 10-Q. The award appears to have forced a comprehensive disclosure audit.

Trigger 3: The Massachusetts AG's Count V. The February 3, 2026 complaint explicitly accuses Bitcoin Depot of deceiving investors by framing known, quantified fraud facilitation as a forward-looking "risk factor." Count V seeks securities-law-style rescission — allowing stock purchasers to tender their shares for a refund. A company facing that theory has every incentive to over-disclose in its next filing to demonstrate good faith.

The 2025 10-K itself acknowledges that disclosure controls and procedures were not effective as of December 31, 2025, and identifies material weaknesses in internal control over financial reporting. That admission does not prove earlier nondisclosure was intentional — but it does provide the company's own explanation for why the reporting environment was weak.

Section 06The Great Retail Dump: $35.1 Million Raised, Compliance Relaxed?

The 2025 10-K confirms that Bitcoin Depot sold 1,295,776 shares of Class A common stock for net proceeds of $35.1 million through its at-the-market equity program in 2025. As of December 31, 2025, $14.9 million of the $50 million ATM program remained available. The company acknowledges it is now subject to the "baby shelf rule," which caps future shelf offerings at one-third of public float in a 12-month period.

This $35.1 million equity raise occurred against the backdrop of: total distributions to BT Assets of $10.1 million in 2025 (plus the $8.4M TRA termination); a $29 million preferred distribution paid to Mintz in December 2024; Mintz simultaneously operating a 12-million-share selling plan; and an $18.5 million arbitration liability disclosed only after the primary equity offering closed. The capital raise was the mechanism that refilled the hole the distributions had created.

The $2.2M vs. $8.4M discrepancy. Bitcoin Depot's May 30, 2025 press release emphasized that the Up-C restructuring "extinguishes the $2.2 million Tax Receivable Agreement liability" — framing it as a small obligation being cleaned up. The 8-K filed the same day explicitly states: the company made a cash payment of $8,400,000 to former stockholders of BT Assets (including Mintz). The gap between the public-facing characterization and the actual SEC disclosure illustrates the pattern this investigation documents.

The Massachusetts Attorney General alleges Bitcoin Depot weakened compliance safeguards between 2021 and 2023 to drive up transaction volumes. The financial pressure of the Buchanan/Mintz payout structure provides a direct motive. Management's own 2026 guidance projects a 30–40% revenue decline, attributed to the "evolving regulatory landscape" and compliance improvements including universal ID verification launched in October 2025 and mandatory ID for all users in February 2026. If fixing compliance destroys a third or more of your revenue, a substantial portion of historical income was derived from activity that now constitutes regulatory violations.

Bitcoin Depot's position: The company has consistently denied wrongdoing, stating it "cannot be held liable for the criminal acts of third-party scammers" and has built its business "around compliance and consumer protection." It implemented mandatory ID verification for new users in October 2025 and for all users in February 2026. Critics note these measures came only after multiple state attorney general actions. The company says it "strongly disagrees" with the allegations in the Massachusetts and Iowa complaints and intends to defend itself vigorously.

Section 07Six Questions for Bitcoin Depot

Based on the new filings, Bitcoin ATM News has directed the following questions to Bitcoin Depot's investor relations. We will publish their response, or note their decision not to respond, in a follow-up.

Questions Submitted to Bitcoin Depot Inc.

- Why was Exhibit 10.32 never filed as a required exhibit before? The July 2023 amendment was referenced in narrative compensation disclosure in the FY2024 10-K, demonstrating the company's awareness of the agreement. Yet under Regulation S-K Item 601(b)(10), the underlying document is a required annual-report exhibit for material compensatory arrangements with Named Executive Officers. The first 10-K after the SPAC closing (FY2023) and the FY2024 10-K both omitted it. Was the failure to file the document — while disclosing its existence in narrative form — intentional?

- Did Mintz know TNW was deficient when he signed the bonus? The agreement's $3M TNW trigger implies knowledge that the metric was being tracked. Did any state regulator receive the 2022/2023 audited financials as part of license renewals? Were those submissions accompanied by any disclosures of the deficiency?

- Who authorized the $29M preferred distribution while insolvent? The company was negative equity in 2024. Did it obtain a solvency opinion under Delaware LLC Act Section 18-607? If not, Mintz and the approving officers may face personal liability for the distribution.

- Was the $15M October offering prospectus complete? BitAccess arbitration hearings ran through October 2025. The offering priced October 7. The award came November 24. Was it a "reasonably possible" loss that should have been disclosed in the offering documents?

- What changed to trigger the disclosure flood? Was it Mintz's departure from CEO, Buchanan's new SOX certification exposure, the Massachusetts AG's Count V investor deception theory, or all three?

- Were other states' license renewal applications accurate? Bitcoin Depot operates under money transmitter licenses in 19 states. Those licenses require annual renewal certifications and submission of audited financials. Connecticut confirmed OpCo failed its minimum TNW requirement in 2022 and 2023. Did Bitcoin Depot's renewal applications in those years submit the OpCo audited financials showing TNW deficiency to other state regulators? Were those applications accompanied by compliance certifications? If the answer to either question is no, potential liability may extend well beyond Connecticut.

Section 08The Bottom Line

Bitcoin Depot's March 18 filing doesn't resolve the questions our original investigation raised. It sharpens them. The Buchanan bonus agreement is a contemporaneous, signed document that makes the company's internal priorities legible: management was focused on TNW thresholds and cash distributions to insiders at the same time. The Connecticut order confirms the operating entity was failing its regulatory minimum. The litigation disclosure explosion reveals that investors were getting a thinner picture for years — and that fuller disclosure arrived only when a new CEO faced personal certification liability, an arbitration award made nondisclosure untenable, and a state attorney general alleged outright investor deception.

The new filings create a substantial evidentiary basis to ask whether management delayed or minimized disclosure of TNW deficiencies and litigation exposure while raising public capital and facilitating insider cash extraction. That is not a conclusion. It is a question the documents themselves now force — and one that regulators, plaintiffs, and investors will need to answer.

What to watch next: The Canaccord Genuity trial (set for 2027, $0–$23M exposure). The Moe Adham / BitAccess minority shareholder arbitration outcome ($0–$10.4M). Whether other states with active money transmitter licenses — the 10-K lists 19 — initiate proceedings similar to Connecticut's, given that the same audited financials showing deficient TNW were available to all of them. And whether the SEC takes interest in the three-year gap between Exhibit 10.32's execution and its first appearance on EDGAR.

Methodology & Sourcing: This article is based on Bitcoin Depot Inc.'s March 18, 2026 Form 10-K (SEC File No. 001-41672), Exhibit 10.32 thereto, the March 17, 2026 NT 10-K, the March 9, 2026 Connecticut Department of Banking emergency order, the Adham v. BitAccess Statement of Claim (CV-24-00730021, Ontario Superior Court of Justice, filed October 25, 2024), prior SEC quarterly and annual filings, Form 4 insider transaction reports, and the Massachusetts Attorney General's February 3, 2026 complaint. All financial figures are from the company's own SEC filings unless otherwise noted. All allegations from the Adham claim are attributed as such. Bitcoin Depot has been contacted for comment. This is Part 2 of an ongoing investigation.