- ~54% of California kiosk locations are voucher-based, not direct-settlement Bitcoin ATMs

- $8.37M in unredeemed Coinme vouchers booked as revenue per Washington State DFI

- Coinme fined $3.92M by SEC for unregistered UpToken securities offering

- Voucher model creates a custody gap — operator holds cash before Bitcoin is delivered

- Direct-settlement ATMs have no unredeemed balance risk — Bitcoin sent at the machine

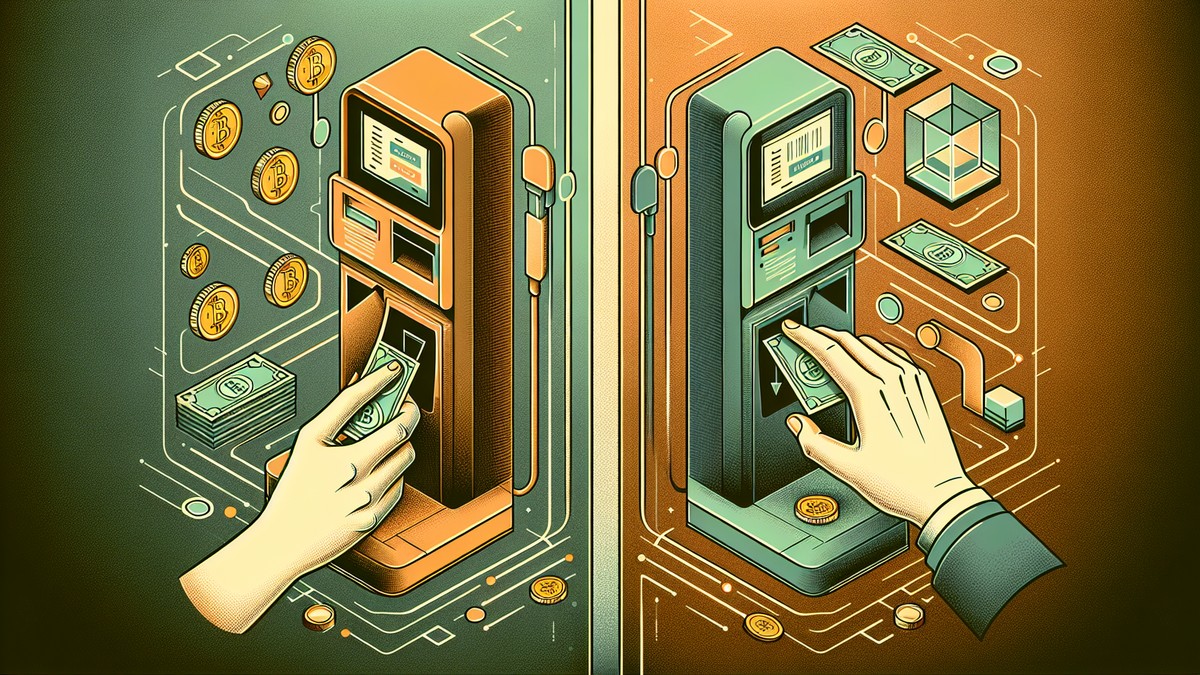

The Bitcoin ATM industry has two fundamentally different models operating under the same regulatory umbrella. One gives you Bitcoin at the machine. The other gives you a receipt and a homework assignment.

Across the United States, thousands of kiosks branded as cryptocurrency access points actually operate as voucher dispensers—machines that accept cash but don't deliver cryptocurrency on the spot. Instead, customers receive a paper voucher with a redemption code and must complete the transaction later through a separate online process. The largest voucher-based network, Coinme, operates through Coinstar coin-counting kiosks at major grocery chains.

This distinction matters far more than most consumers realize. The voucher model creates a custody gap—a period where the operator holds customer funds without delivering the purchased asset—that has already produced real regulatory consequences.

How Direct-Settlement Bitcoin ATMs Work

A direct-settlement Bitcoin ATM operates as a self-contained transaction terminal. The customer approaches the machine, inserts cash, scans a Bitcoin wallet QR code, and the Bitcoin is sent on-chain—typically within minutes. One visit, one machine, one transaction. The customer leaves with cryptocurrency in their own wallet.

This is the model used by operators like Bitcoin Depot, RockItCoin, Coinhub, CoinFlip, Athena Bitcoin, Byte Federal, and America Bitcoin ATM. The hardware is purpose-built: bill validators, receipt printers, and QR scanners in a dedicated enclosure. Many models also support two-way transactions, dispensing cash for cryptocurrency sells.

The key characteristic: no custody gap. Customer funds are converted and delivered during the same visit. The operator never holds customer funds in limbo.

How Voucher Kiosks Work

Voucher-based systems use a fundamentally different approach. The process requires multiple steps, often across multiple days:

The Voucher Purchase Flow:

- Insert cash at a Coinstar kiosk in a grocery store

- Receive a paper voucher with a redemption code printed on the receipt

- Go home and open a web browser or mobile app

- Create an account with the voucher service (if you don't have one)

- Complete identity verification (KYC process)

- Enter the voucher code to claim the cryptocurrency

- Wait for delivery of the cryptocurrency to your wallet

The customer leaves the kiosk with a piece of paper, not Bitcoin. Settlement happens later—after the customer completes account creation, identity verification, and code redemption through a separate platform. If a customer loses the voucher, forgets about it, or fails to complete the online steps, their cash sits with the operator indefinitely.

The Core Problem: Custody Without Settlement

The voucher model's fundamental weakness is the gap between payment and delivery. When a customer inserts $200 into a Coinstar kiosk and walks away with a voucher, the operator has $200 of customer funds with no corresponding cryptocurrency transaction completed.

What happens to unredeemed vouchers?

- Customer funds in limbo: Cash collected, cryptocurrency not delivered—the operator holds the money

- Unclaimed property liability: State laws require unredeemed balances to be escheated (turned over to the state) after a dormancy period

- Revenue recognition temptation: Operators may be tempted to book unredeemed vouchers as income—exactly what Washington state regulators found Coinme doing

- No customer recourse at the kiosk: If something goes wrong with the online redemption process, the customer can't return to the kiosk for help

Direct-settlement ATMs don't have this problem. There's no custody gap, no unredeemed balance pool, and no unclaimed property liability. The customer's Bitcoin is in their wallet before they leave the store.

Regulatory Risk Comparison

| Risk Factor | Voucher Systems | Direct-Settlement ATMs |

|---|---|---|

| Customer fund custody | High — operator holds funds between purchase and redemption | Low — funds converted and sent on-chain immediately |

| Unclaimed property exposure | Yes — unredeemed vouchers create escheatment liability | No — funds in customer wallet, no residual balance |

| Settlement timing | Hours to days (requires online redemption) | Minutes (on-chain confirmation) |

| User experience | Multi-step, multi-device, requires internet access | Single visit, single device, self-contained |

| Customer support complexity | Higher — issues span kiosk + online platform | Lower — all issues are machine-related |

| Primary regulatory issues | Fund custody, unclaimed property, securities risk | Fee transparency, fraud prevention, AML compliance |

Both models face regulatory scrutiny, but the nature of the risk differs substantially. Direct-settlement operators' enforcement actions typically involve fee transparency violations (charging above state-mandated caps) and anti-money laundering compliance. Voucher operators face those same risks plus additional exposure around fund custody and unclaimed property—a category of risk that direct-settlement machines simply don't create.

Case Study: Coinme's Enforcement Record

Coinme, Inc. is the largest voucher-based cryptocurrency kiosk operator in the United States, operating through a partnership with Coinstar that places crypto purchasing capabilities in thousands of grocery store coin-counting kiosks. The company's regulatory history illustrates the risks specific to the voucher model.

SEC UpToken Settlement (April 2023)

In April 2023, the SEC settled charges against Coinme, its subsidiary Up Global SEZC, and CEO Neil Bergquist for conducting an unregistered securities offering through a token called "UpToken." The SEC found that the entities raised approximately $3.5 million from investors between October and December 2017 without registering the securities.

SEC Enforcement Action

Washington State DFI Cease-and-Desist (December 2025)

In December 2025, the Washington State Department of Financial Institutions (DFI) issued a cease-and-desist order against Coinme based on findings directly tied to the voucher model's custody risk. State examiners found that Coinme had accumulated approximately $8.37 million in unredeemed customer vouchers—$2.2 million from Washington customers in 2023 and $6.17 million from 2024—and was treating those funds as company revenue rather than customer liabilities. The DFI also found Coinme had failed to maintain legally required financial reserves from 2020 through 2025.

The $8.4M Unredeemed Voucher Problem

Washington regulators found Coinme held $8.37 million in customer funds from unredeemed vouchers that the company had booked as income. The DFI imposed a $300,000 fine, sought a 10-year ban on CEO Neil Bergquist from the industry, and moved to revoke Coinme's money transmitter license. Coinme resumed operations on December 30, 2025 under a temporary consent order.

This specific failure mode—unredeemed customer funds treated as company income—is structurally impossible with direct-settlement Bitcoin ATMs, where funds are converted to cryptocurrency and sent to the customer's wallet during the same transaction.

The Washington enforcement action represents the clearest illustration of why the voucher model creates risks that direct-settlement ATMs avoid entirely. When a customer inserts cash into a direct-settlement Bitcoin ATM, there's nothing to "go unredeemed"—the Bitcoin is sent immediately. There is no pool of customer funds sitting on the operator's books.

California DFPI Consent Order (June 2025)

Even California's own financial regulator—the DFPI that registers these kiosks—has taken enforcement action against Coinme. In June 2025, the DFPI issued its first-ever enforcement action under the Digital Financial Assets Law, finding that Coinme had exceeded the $1,000-per-customer-per-day transaction limit, issued over 4,050 receipts missing required disclosures, and exceeded statutory fee maximums. The DFPI imposed a $300,000 fine and ordered $226,700 in total restitution to California consumers.

Zero Hash and the "CINQ by Coinstar" Model

California DFPI registration data lists Zero Hash LLC as one of the largest kiosk operators in the state by location count. Zero Hash is not itself an ATM operator—it's a crypto infrastructure company that provides the settlement layer for "CINQ by Coinstar," a newer voucher-based product. Zero Hash processes the cryptocurrency transactions that occur when customers redeem their vouchers online.

From the consumer's perspective, the experience is similar to Coinme: insert cash at a Coinstar kiosk, receive a voucher, redeem online later. The same custody gap exists, and the same unclaimed property risks apply.

Why This Matters: The California Data

California's Department of Financial Protection and Innovation (DFPI) publishes a registry of all licensed digital financial asset kiosk operators. Analysis of this registry reveals the scale of the voucher/direct-settlement split:

- ~4,650 total registered kiosk locations in California

- ~2,500 (~54%) are voucher-based kiosks (Coinme Inc. + Zero Hash LLC)

- ~2,100 (~46%) are direct-settlement Bitcoin ATMs operated by companies like Bitcoin Depot, CoinFlip, RockItCoin, Athena Bitcoin, and others

More than half of the kiosk locations registered with California's financial regulator are voucher kiosks, not Bitcoin ATMs. When industry statistics cite total "Bitcoin ATM" counts, they often include these voucher kiosks—inflating the apparent size of the direct-settlement market and obscuring the differences in customer experience and risk profile.

Why this site excludes voucher kiosks from listings: BitcoinATM.news lists only direct-settlement Bitcoin ATMs—machines that deliver cryptocurrency to the customer's wallet during the same visit. Voucher kiosks are excluded from our directory because they don't provide the immediate, self-contained Bitcoin purchasing experience that the term "Bitcoin ATM" implies. We track voucher kiosk data from regulatory sources for analysis purposes, but these locations do not appear in our public ATM map or location pages. For more on Coinme's voucher model, see our Coinme information page.

What Consumers Should Know

When you use a direct-settlement Bitcoin ATM, your Bitcoin is yours the moment you leave the machine. With a voucher, you're trusting the operator to honor that piece of paper—and to hold your cash securely until you complete the online redemption process. Coinme's enforcement record—$3.92 million in SEC penalties, $8.37 million in unredeemed customer vouchers booked as income, and $526,700 in California fines and restitution—demonstrates the real-world consequences of that trust.

Neither model is free of regulatory risk. Direct-settlement operators face their own enforcement actions, primarily around fee transparency and anti-money laundering compliance. But the voucher model introduces an additional category of risk—customer fund custody—that has already produced material harm to consumers.

Consumers looking to purchase Bitcoin at a physical kiosk should understand which model they're using before inserting cash. If you're at a Coinstar machine, you're using a voucher system. If you're at a purpose-built Bitcoin ATM from operators listed on this site, you're using direct settlement.

The difference between walking away with Bitcoin and walking away with a receipt is not trivial.